1Chapter 4: Adoption & Implementation of AI¶

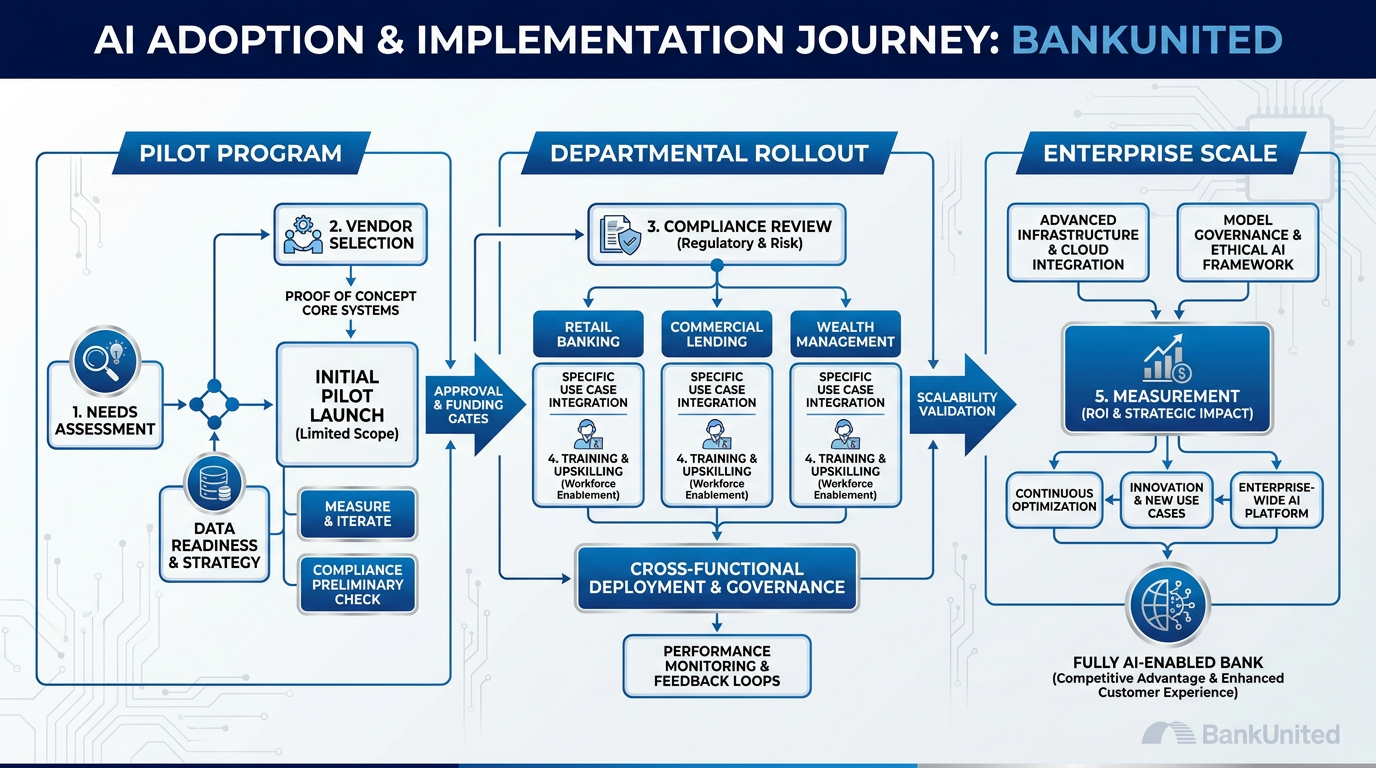

Figure 1:The path from pilot to enterprise is not a straight line. But it has a known shape — and the organizations that navigate it successfully share specific structural choices in common.

“The measure of intelligence is the ability to change.” — Albert Einstein

Most AI programs inside financial institutions die at the same place.

They run a pilot. The pilot succeeds. People are impressed. Leadership is encouraged. And then — almost universally — the pilot sits in presentation slides for six months while governance teams, IT, compliance, and legal work through their respective concerns, and the momentum built by the pilot slowly evaporates under the weight of daily operations.

The technology worked. The people believed in it. The ROI was there to be captured.

And still — nothing scaled.

This is the most important implementation problem in banking AI today. Not the technical problem. Not the model selection problem. Not even the compliance problem, which is more navigable than most people believe. The scaling problem: how do you take a thing that works in one pocket of the organization and make it the way everyone works?

This chapter is the strategic answer to that question. It covers the state of AI in financial services right now — where your peers and your competitors actually are — the known shape of the curve from pilot to enterprise, the regulatory environment that governs AI in banking, the Microsoft platform architecture that makes Copilot the right implementation choice for BankUnited, the risk framework you need, the organizational structure that makes adoption sustainable, and the economics that make the case to leadership.

By the end of this chapter, you will have a complete strategic picture. And you will have built your personal “AI Adoption One-Pager” — the single-page document that names your workflow, your metrics, your risks, and your timeline. That document is the seed of your Showcase Project. And it starts here.

1.11. The State of AI in Financial Services — 2026¶

Let’s establish the baseline. Where are banks actually, right now, in their AI journeys? Not the marketing version — the operational reality.

Figure 2:The AI adoption curve in financial services — 2026. The early movers have 18–24 months of operational learning that late movers cannot buy. The question is which tier BankUnited is determined to occupy.

The early movers have established durable advantages.

JPMorgan Chase has publicly disclosed deploying AI across over 400 distinct use cases, with over 200,000 employees using AI-assisted tools. Their AI investments are generating measurable returns in fraud detection, credit underwriting, document summarization, and client communications. They have an AI Council with direct board-level accountability.

Goldman Sachs has embedded AI into their developer workflows, their research production, and their client-facing communications. Morgan Stanley’s AI-powered wealth management assistant has been adopted by over 98% of their 16,000 financial advisors — not because it was mandated, but because it measurably improved the quality of client conversations.

Wells Fargo, Bank of America, and Truist have each announced significant AI programs with hundreds of millions in committed investment and measurable early returns.

The mid-tier is where the strategic opportunity lives.

Here is what the early movers’ experience has established: the first-mover advantage in banking AI is real, but it is not permanent at the top-tier level. The tools are available to everyone. The regulatory environment is navigating to workable guidance. The primary differentiator is now not access to AI, but organizational capability — the learned ability to deploy it effectively.

For BankUnited, this is the moment. Not because BankUnited is late — the bank is well-positioned relative to its community bank and regional bank peers. But because the window for building organizational AI capability before it becomes table stakes for competitive banking is measured in months, not years.

The regulatory environment is clarifying.

For the first two years of the generative AI era (2023–2024), banking regulators were largely in observation mode — watching, asking questions, issuing guidance that was more principle-based than prescriptive. In 2025 and into 2026, that has changed. There is now meaningful, specific regulatory guidance from all three major federal banking supervisors, and understanding that guidance is essential for any bank running an AI program.

1.22. The Pilot-to-Enterprise Curve — Why Pilots Stall¶

Before we go into the regulatory environment, let’s name the structural reason most AI pilots fail to scale. Understanding this pattern is the prerequisite to avoiding it.

Figure 3:The Valley of Death is not inevitable. But it is the default. Every organization that has successfully scaled past it made specific structural choices that others did not.

The curve has a known shape:

Phase 1 — The Pilot Peak: Enthusiasm is high. A small team runs a focused experiment. Results are real and visible. Champions are energized. Leadership is encouraged.

Phase 2 — The Valley of Death: The pilot moves from the experiment phase to the “what do we do with this now?” phase. IT needs to assess security. Compliance needs to review the workflow. Legal needs to weigh in on data handling. Someone in procurement wants to renegotiate the vendor contract. Meanwhile, the team that ran the pilot goes back to their regular jobs, because there is no structure for sustaining momentum. Three months pass. The pilot deck sits on a SharePoint page. Nobody mentions it at the next all-hands.

Phase 3 — Enterprise or Flatline: Organizations that built the right structures — a governance framework that was ready for the pilot results, a Champion network that could absorb the learnings, a leadership decision to fund the next phase before the first phase ended — scale through the Valley. Organizations that didn’t build those structures flatline. The AI program gets quietly deprioritized.

The structural choices that separate scalers from flatliner:

Governance framework exists before the pilot launches, not after. The pilot findings slot into a pre-built review process rather than triggering a new governance conversation from scratch.

The next phase is funded before the current phase ends. Momentum is the most fragile resource in any change program. Gaps in commitment are where momentum dies.

The pilot is designed to produce a workflow template, not just a result. The goal is not “show it works” — it is “build the repeatable pattern that other teams can adopt.”

Champions are organized into a named community before the pilot ends. The learning does not live in the pilot team. It lives in a structured network.

These are not complicated. They are not expensive. They are, however, decisions that have to be made deliberately — because the default path leads straight into the Valley.

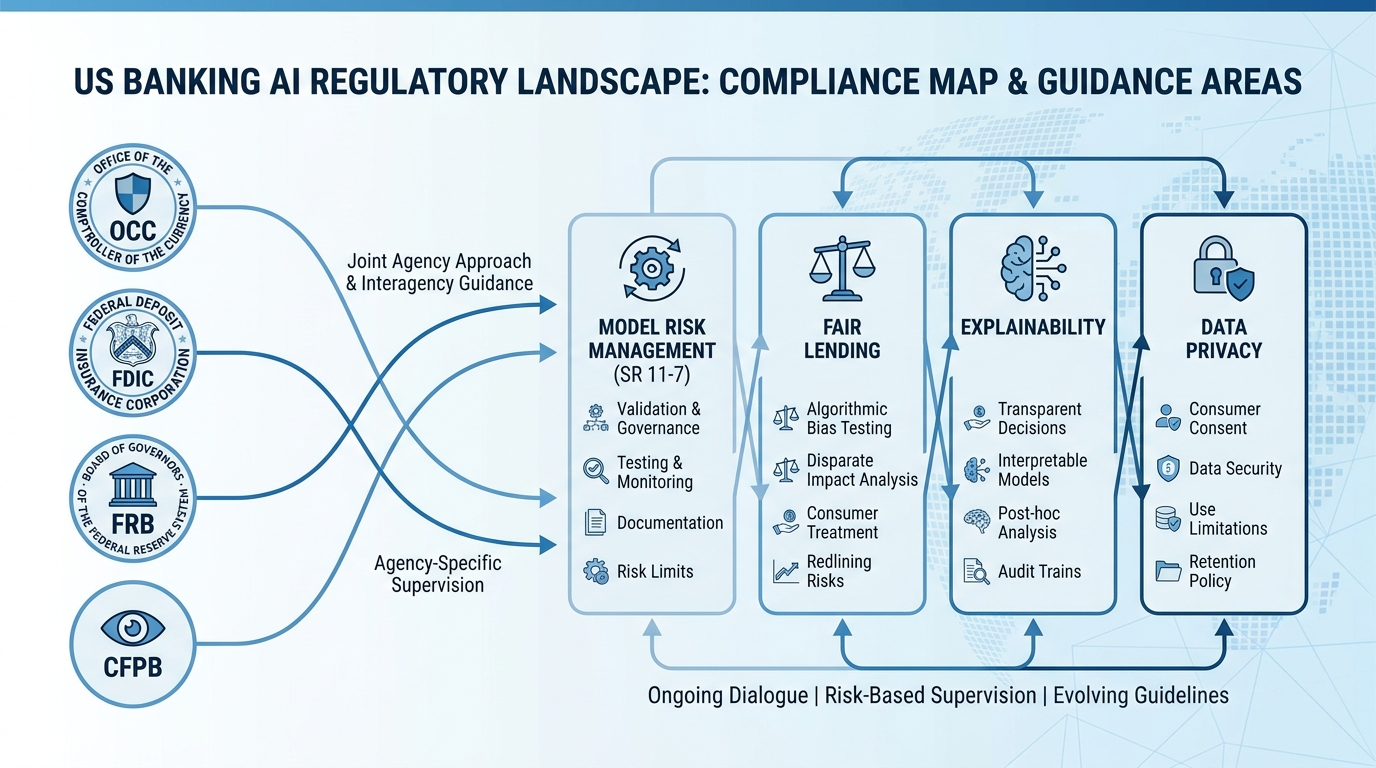

1.33. The Regulatory Environment — What Every BankUnited Professional Needs to Know¶

Let us be specific about the regulatory landscape, because this is the area where the most confusion — and the most unnecessary fear — lives inside banking organizations running AI programs.

Figure 4:Four regulators, one direction: AI use in banking must be safe, fair, transparent, and explainable. Microsoft Copilot’s enterprise architecture was designed with these requirements in mind.

1.3.1OCC — The Comptroller’s Guidance¶

The Office of the Comptroller of the Currency has been the most active of the federal banking regulators on AI. Their guidance establishes several principles that map directly to how BankUnited should structure its Copilot program:

Model risk management (MRM) applies to AI models. If an AI model is used in credit decisions, fraud detection, or other material banking judgments, it falls under the OCC’s MRM framework — the same framework that governs statistical credit scoring models. This means validation, documentation, ongoing monitoring, and governance. Note: Copilot used for document drafting, meeting summarization, or communication assistance does not constitute a model under MRM guidance. The requirement kicks in when AI output directly drives a material banking decision.

Third-party risk management applies to AI vendors. Using a third-party AI platform — including Microsoft Copilot — falls under the OCC’s third-party risk guidance. This means BankUnited’s vendor management process needs to include an assessment of Microsoft as an AI vendor. Microsoft’s enterprise agreements and compliance documentation are designed specifically for this review.

Fair lending laws apply to AI in credit decisions. If AI is used in any aspect of the credit underwriting or decisioning process, Equal Credit Opportunity Act (ECOA) and Fair Housing Act obligations apply in full. AI does not create exceptions to fair lending. It creates new monitoring requirements.

1.3.2Federal Reserve — The Safety and Soundness Framework¶

The Federal Reserve’s AI guidance is organized around its existing safety and soundness framework — which means the standard is not “is this AI use legal?” but “is this AI use consistent with safe and sound banking practices?”

Under this framework, the Fed is primarily concerned with:

Operational resilience: Does AI use create new operational risks? How are those risks monitored and controlled?

Model governance: Are material AI models validated, documented, and regularly reviewed?

Board accountability: Does the board have appropriate visibility into material AI uses and their associated risks?

The Federal Reserve has been explicit that supervised institutions are expected to have AI governance policies proportionate to their AI footprint — and that “we don’t have an AI policy” is not an acceptable answer as of 2026.

1.3.3FDIC and CFPB — Consumer Protection Dimensions¶

The FDIC’s AI focus is primarily on consumer protection and safety in community banking contexts — ensuring that AI used in retail banking decisions does not create disparate impact or undermine consumer protections.

The CFPB has been the most aggressive of the federal regulators in focusing on AI explainability — specifically, the requirement under the Equal Credit Opportunity Act that adverse action notices provide specific, accurate reasons for credit denials. An AI model that generates a credit decision without producing an explainable, adverse-action-compliant rationale fails this requirement, regardless of its accuracy.

1.3.4What This Means for Your Day-to-Day Copilot Use¶

For the vast majority of Copilot use cases in this master class — drafting documents, summarizing meetings, researching industries, preparing client briefs, building Excel analyses — the regulatory considerations above do not directly apply. Those activities are professional productivity tools, not model-driven banking decisions.

The regulatory framework becomes directly relevant when Copilot (or any AI) is used in:

Credit underwriting or credit decisioning

Fraud detection or anti-money laundering

Customer screening or risk rating

Any consumer-facing automated decision

For those workflows, BankUnited’s compliance, risk, and legal teams should be the first call — before implementation, not after.

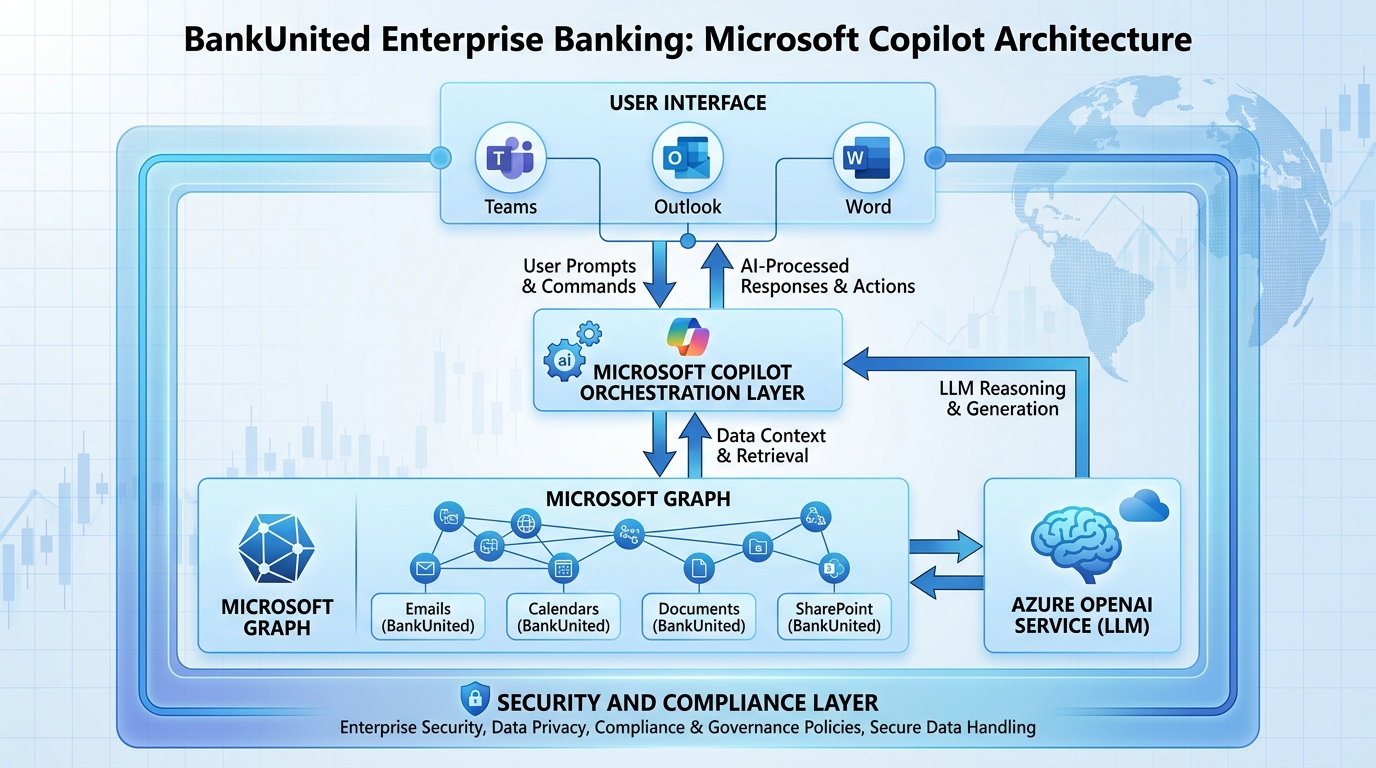

1.44. Microsoft Copilot as the Implementation Platform — Why M365 Is the Right Home¶

Given the regulatory environment just described, the question “which AI platform should BankUnited use?” is not primarily a technology question. It is primarily a governance and compliance question.

And on that dimension, Microsoft 365 Copilot has specific architectural advantages over generic AI tools that are worth understanding in detail.

Figure 5:Microsoft 365 Copilot’s architecture was designed for regulated enterprise environments. The compliance infrastructure is not added on — it is foundational.

Your data does not train the model. This is the first and most important architectural point for a bank. When BankUnited professionals use Microsoft 365 Copilot, their prompts, their data, and their outputs are not used to train Microsoft’s underlying AI models. The conversations and data stay within BankUnited’s Microsoft 365 tenant — protected by the same enterprise data boundary that governs all M365 data.

Permission inheritance is automatic. As established in Chapter 1: Copilot can only access data that the user themselves can access. Restricted SharePoint sites, confidential email threads, protected documents — the AI respects the same access controls that BankUnited’s IT team has configured. A Copilot agent cannot surface information that the requesting user would not be permitted to see manually.

Every interaction is logged. Microsoft 365 Copilot maintains audit logs of all interactions within the Microsoft Purview compliance infrastructure. This is not a privacy concern — it is a compliance asset. If a regulator ever asks “what AI interactions produced this document?” — the answer is retrievable. BankUnited’s IT and compliance teams can access these logs through Microsoft Purview.

Sensitive information labels are respected. Documents marked as Confidential, Highly Confidential, or otherwise restricted under Microsoft Information Protection (MIP) are handled according to those labels in Copilot interactions. AI does not bypass information protection classifications.

The data never leaves your Microsoft 365 tenant. All Copilot processing happens within Microsoft’s commercial data processing infrastructure — the same environment that Microsoft uses for all enterprise M365 data. Data does not transit to consumer AI services. Prompts and responses do not go to OpenAI’s consumer infrastructure.

These architectural features map directly to the regulatory requirements above: data protection satisfies OCC third-party risk requirements. Audit logging satisfies the Federal Reserve’s operational documentation expectations. Permission inheritance prevents unauthorized data exposure. Information protection labels help enforce data governance policies.

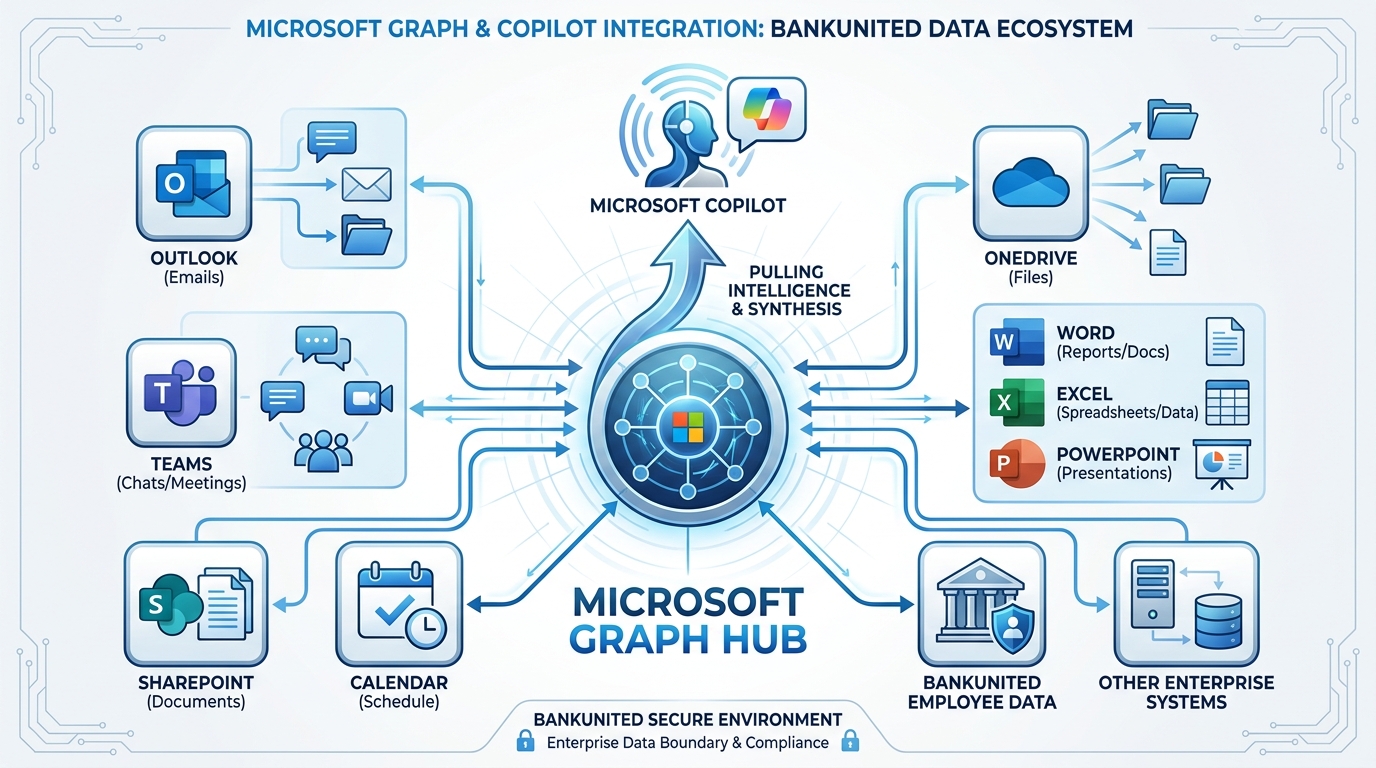

1.55. Microsoft Graph and Work IQ — Your AI Already Knows Your Work¶

Figure 6:Microsoft Graph is the connective tissue between Copilot and your entire M365 ecosystem — emails, documents, meetings, and files — making your AI contextually aware of your actual work.

One of the most underappreciated aspects of Microsoft 365 Copilot’s architecture is what Microsoft calls the Microsoft Graph — the data layer that connects all M365 services and makes your Copilot contextually aware of your actual work.

The Microsoft Graph is the technical infrastructure that answers the question: “How does Copilot know about my emails and calendar without me having to tell it?”

The Graph is a vast, continuously updated data model of your work activity across all M365 services: who you email, what documents you work on, what meetings you attend, what topics appear in your Teams conversations, what files you have recently accessed, and the relationships between all of these. It is, in effect, a real-time map of your professional context.

Work IQ is the applied intelligence layer built on top of the Graph. When you ask Copilot “What are the key decisions from my last three meetings with the Henderson account?” — Work IQ is what makes that question answerable. It traverses the Graph to find the relevant meetings, access the transcripts if available, identify the decisions, and present them in a coherent summary — without you having to specify any file paths, dates, or document names.

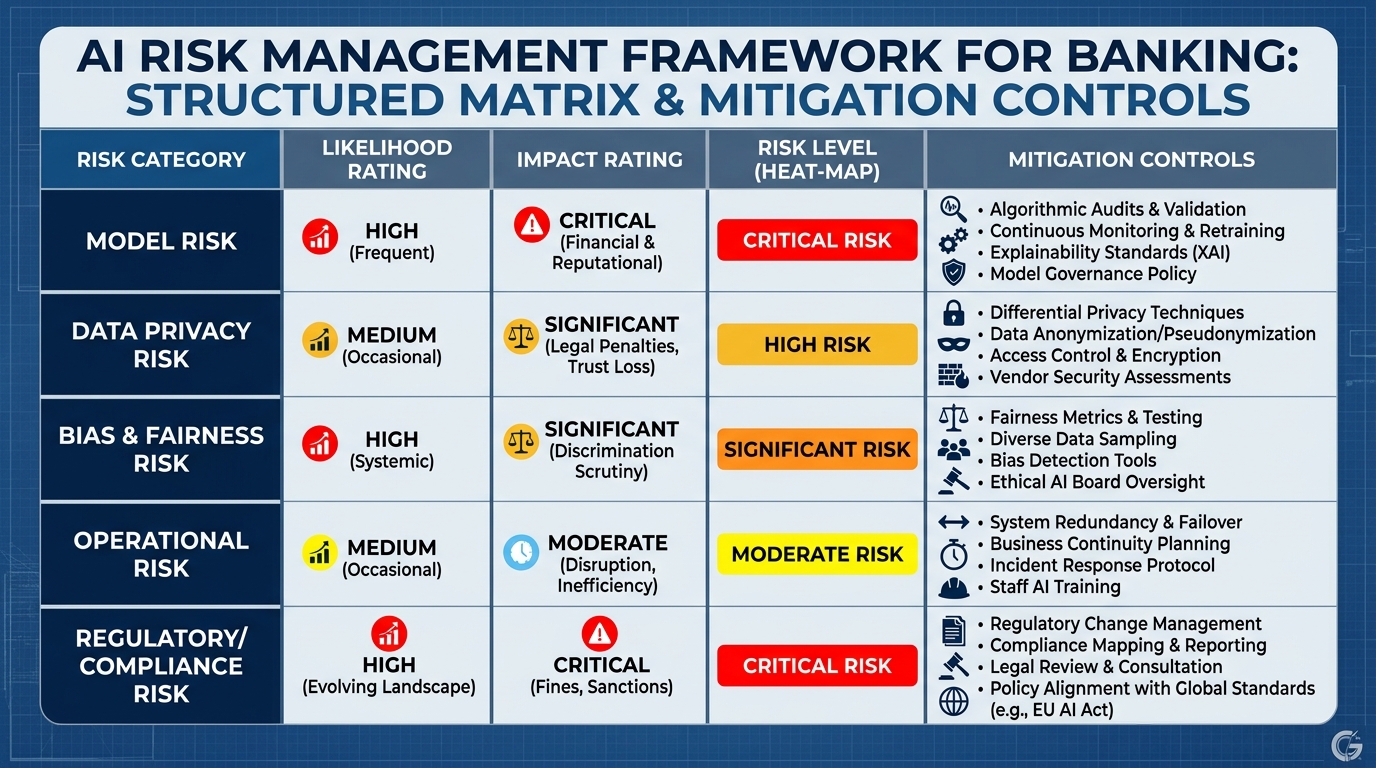

1.66. Risk Frameworks for AI — The Four Dimensions BankUnited Must Manage¶

With the regulatory landscape understood and the platform architecture established, let’s get specific about the risk dimensions that BankUnited’s AI program needs to manage. These are not hypothetical risks — they are the ones that have actually materialized in banking AI deployments and have appeared in regulatory exam findings.

Figure 7:The four AI risk dimensions in banking — each real, each manageable with the right controls. Understanding them is the prerequisite to deploying AI responsibly.

1.6.1Risk 1: Data Leakage¶

What it is: Sensitive information from one context being exposed inappropriately in another context, or being exposed to external parties.

In banking specifically: Client PII appearing in AI outputs that are shared inappropriately; confidential deal information surfacing in Copilot responses accessed by users without appropriate authorization; AI-assisted documents containing embedded proprietary data being shared outside the intended audience.

The Copilot control: Permission inheritance (only surfaces data the user can access), enterprise data boundary (data doesn’t leave the M365 tenant), Information Protection label enforcement. The primary control, however, is human: professionals must apply the same judgment about what to include in AI prompts as they would about what to include in any communication.

1.6.2Risk 2: Hallucination¶

What it is: AI generating factually incorrect information with apparent confidence. The model “hallucinates” — producing text that sounds plausible but is fabricated, citing sources that don’t exist, or stating numbers that are wrong.

In banking specifically: A credit memo with a hallucinated financial ratio. A client brief with incorrect regulatory references. A compliance document citing a guidance that doesn’t exist in the stated form.

The Copilot control: Grounding — Copilot is designed to source responses from your actual Microsoft 365 data when performing work tasks, reducing (but not eliminating) hallucination. The primary control is human: every AI-generated factual claim in a document intended for external use or material internal decision-making must be verified by a qualified professional before the document leaves their hands.

1.6.3Risk 3: Bias¶

What it is: AI systems producing outputs that reflect biases present in training data, leading to systematically different treatment of different groups.

In banking specifically: Credit analysis tools that underweight applications from protected class applicants due to patterns in historical training data; marketing tools that generate different messaging for different demographic groups in ways that violate fair lending principles; hiring tools that exhibit differential outcomes.

The Copilot control: For general productivity use (drafting, summarizing, analyzing), bias risk is low. For any AI use in credit-adjacent workflows, formal bias testing and ongoing monitoring are required under the regulatory framework described above. Human review at every credit-adjacent output is mandatory, not optional.

1.6.4Risk 4: Model Drift¶

What it is: An AI model’s performance degrading over time as the real world changes in ways not reflected in the model’s training data.

In banking specifically: A fraud detection model trained on pre-pandemic transaction patterns performing poorly as transaction behavior has permanently changed. A credit scoring model trained on one interest rate environment underperforming in a dramatically different rate environment.

The Copilot control: For generative AI productivity use (Copilot for drafting, summarizing, analysis), model drift is managed by Microsoft through their continuous model updates. For any specialized AI models deployed by BankUnited for material banking decisions, model monitoring and periodic revalidation are regulatory requirements.

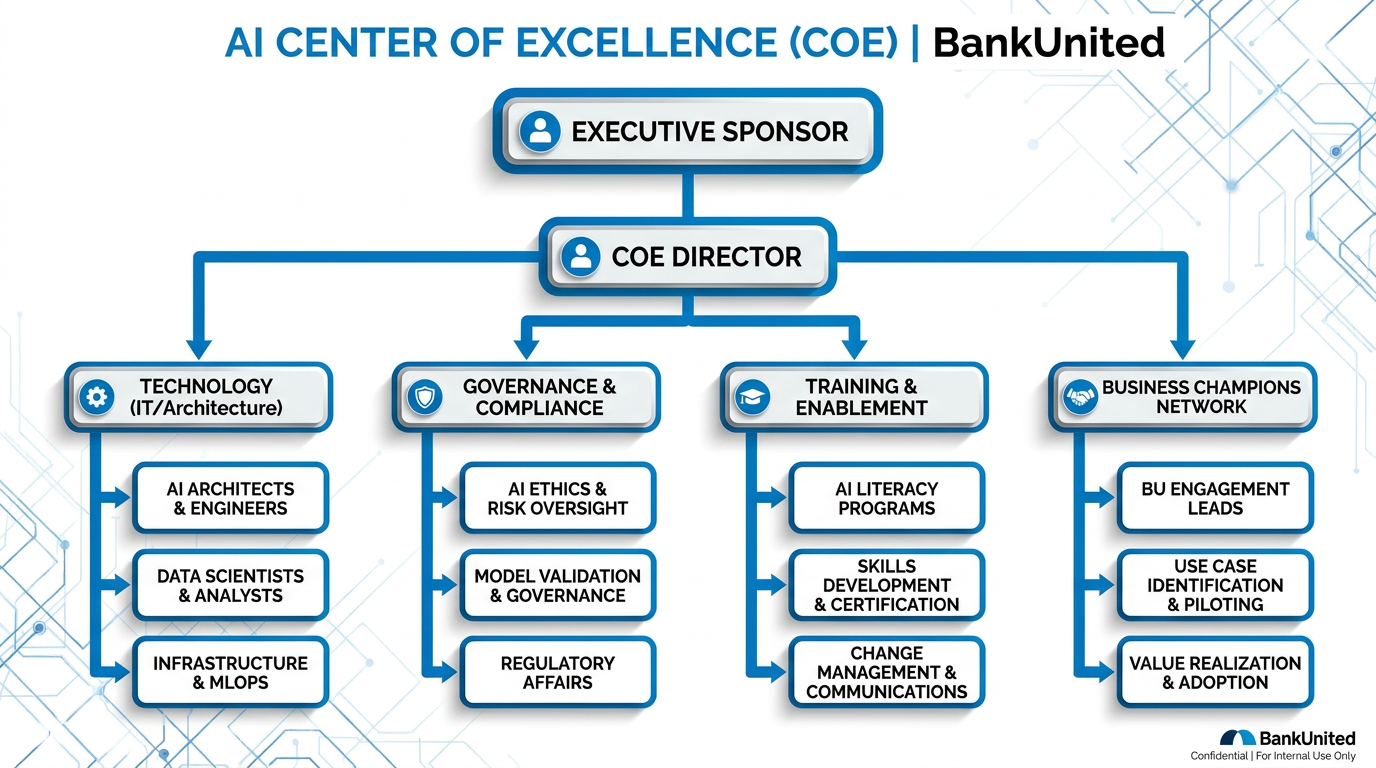

1.77. Building an AI Center of Excellence at BankUnited¶

An AI Center of Excellence (CoE) is not a department. It is a coordination function — a lightweight organizational structure that prevents the AI program from fragmenting into disconnected departmental initiatives, each reinventing the wheel, each creating redundant governance work, and none of them sharing the learnings that compound over time.

The CoE does not do AI work. It enables AI work. The distinction matters.

Figure 8:The AI Center of Excellence is not where AI happens. It is the infrastructure that makes AI happen well — across departments, at scale, with shared learning and consistent governance.

Core roles in the BankUnited CoE:

Executive AI Sponsor — A senior leader (ideally C-suite or direct report) who provides organizational visibility and accountability for the AI program. Their job is not operational. It is to ensure that AI adoption remains a strategic priority, that resourcing decisions are made, and that the program has the cross-functional authority to move things when they get stuck.

AI Program Lead — The operational coordinator of the CoE. Manages the Champion network, coordinates governance reviews, tracks the portfolio of AI initiatives, owns the communication calendar, and serves as the organizational connective tissue between IT, compliance, and business units.

IT Representative — Owns the technical infrastructure: Microsoft 365 tenant configuration, Copilot licensing and access, security architecture review, and integration with BankUnited’s existing technology stack.

Compliance/Risk Representative — The governance translator: maps AI use cases to the regulatory framework, provides input on acceptable use policies, escalates cases that require formal model risk management, and maintains the approved use case library.

Departmental Champions — The existing Champion network from Chapter 3, organized into the CoE’s extended team. Each Champion is the CoE’s eyes and ears in their department — surfacing what is working, what is stalling, and what new use cases are emerging.

The three operating cadences:

Table 1:AI CoE Operating Cadences

Cadence | Participants | Agenda | Frequency |

|---|---|---|---|

Executive Review | Sponsor + Program Lead + Business Heads | AI portfolio review, strategic priorities, resource decisions | Monthly |

Operational Sync | Program Lead + IT + Compliance + Champions | Pilot updates, governance queue, shared learnings, blocker resolution | Bi-weekly |

Champion Community | All Champions + Program Lead | What’s working, what’s not, prompt library updates, peer support | Weekly (async-first, with optional live session) |

The CoE does not need to be large to be effective. At BankUnited’s scale, a part-time Program Lead, one IT resource, one Compliance/Risk resource, and an active Champion network is sufficient to run a high-functioning AI program. The leverage is in the coordination and the shared learning — not in headcount.

1.88. The Economics — Making the Case for AI Investment¶

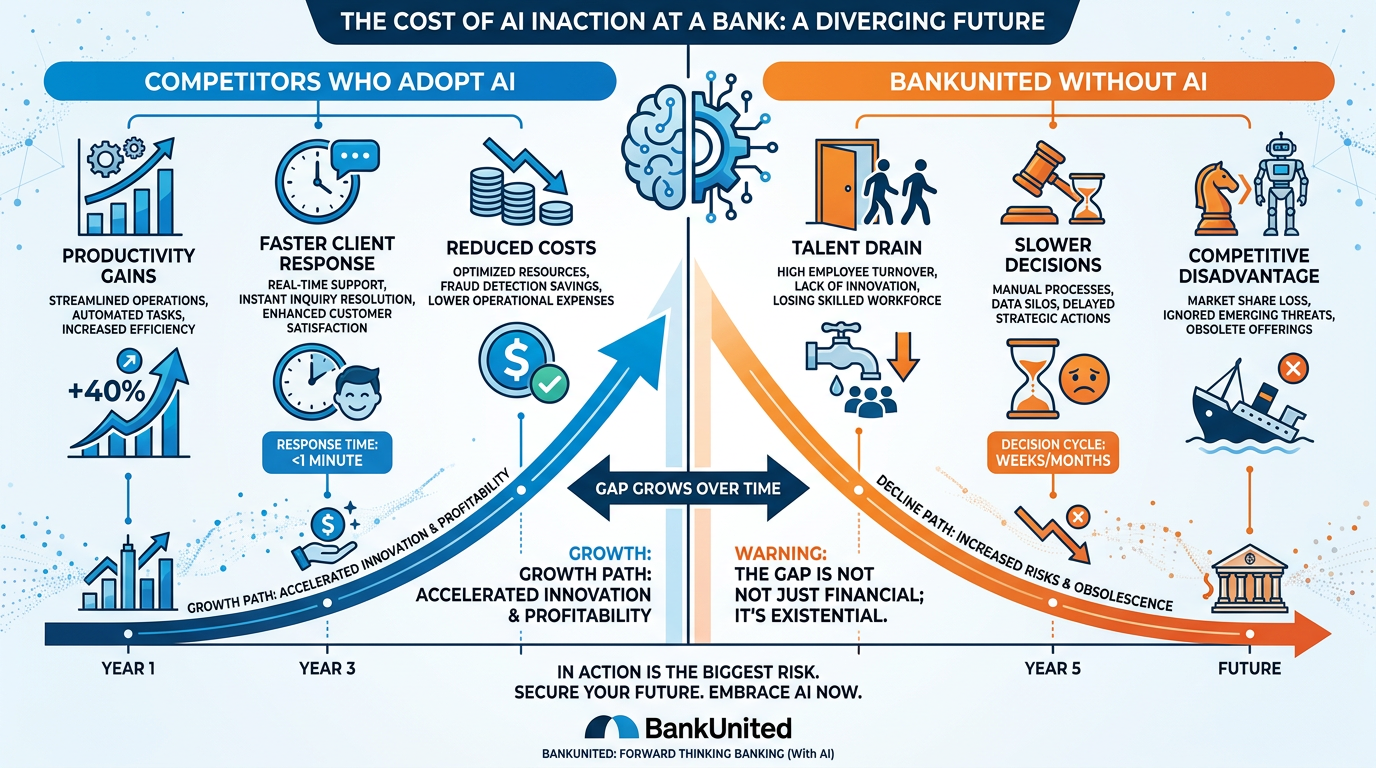

Figure 9:The cost of inaction compounds over time — banks that delay AI adoption fall further behind competitors on speed, productivity, and talent retention with every passing quarter.

We have covered the technology, the regulation, the architecture, and the organizational structure. Now let’s talk about money — because every investment at BankUnited requires a defensible return, and AI is no exception.

Figure 10:The economics of banking AI are compelling on three dimensions: time-savings ROI, revenue impact, and cost of inaction. Each dimension alone justifies investment. Together, they make inaction the riskier choice.

1.8.1The Time-Savings ROI¶

PwC’s analysis found that professionals who consistently apply AI to their knowledge work recapture an average of 47% of previously consumed task time. Let’s put BankUnited numbers around that.

A relationship manager at BankUnited might spend:

2 hours per week researching and preparing for client meetings

3 hours per week drafting client communications (emails, memos, summaries)

2 hours per week compiling and formatting reports

1.5 hours per week in meeting preparation and follow-up documentation

That is 8.5 hours per week of work that Copilot can materially accelerate. At a 47% efficiency gain, that is 4 hours per week recovered — time that can be reinvested in additional client relationships, deeper client interactions, or strategic work that was previously crowded out.

Four hours per week, per RM, at a conservative loaded hourly rate of 340 per RM per week, $17,000 per RM per year. Multiply by the number of relationship managers at BankUnited, and the numbers become significant quickly — and that is one role in one function.

1.8.2The Revenue Impact¶

McKinsey’s research on AI-augmented relationship management in banking found that RMs using AI assistance consistently for client preparation, communication, and follow-up showed measurable improvements in client retention, wallet share growth, and new client acquisition rates — with the typical AI-augmented RM managing 15–20% more client relationships than their non-augmented peers.

For BankUnited, with a relationship-centric business model and a client base that values the quality of their banking relationships above branch convenience or rate alone, this dimension of the ROI may be the most meaningful. If AI allows each RM to deepen more relationships with the same or less effort, the revenue compounding effect is significant and durable.

1.8.3The Cost of Inaction¶

This is the analysis that does not appear in most ROI models but should. The question is not just “what is the return on AI investment?” but “what is the cost of not investing?”

As early-mover banks continue to build AI capability, two things happen simultaneously. Their costs decrease — because AI-assisted professionals are more efficient, and that efficiency compounds over time. And their client experience improves — because AI-augmented RMs are better prepared, more responsive, and capable of managing more complex relationships.

For a bank competing for the same clients in the same South Florida market, the competitive consequence of a 24-month delay in AI capability development is not a missed quarter. It is a compounding disadvantage that gets harder to close with every passing month.

The BCG analysis framing is the most useful here: AI leaders generate 1.7× the revenue growth of AI laggards. Not as a one-time event — as a sustained divergence. The gap widens over time, not closes. Inaction is not a neutral choice. It is a choice to be on the losing side of that divergence.

1.9🧪 Try This — Build Your AI Adoption One-Pager¶

This is the exercise that the rest of the program builds toward. The AI Adoption One-Pager is a single page that captures your personal roadmap for applying everything in Part I of this book to one specific, real workflow at BankUnited.

It is the seed of your Showcase Project. It is the document you will bring to your manager in a 1:1. It is the thing that transforms this master class from interesting reading into a professional development commitment.

1.10Chapter Summary¶

Chapters 1 through 4 form a complete foundation.

Chapter 1 gave you the conceptual framework — the LLM, context engineering, the flashlight, the persona, meta-prompting, and agents. Chapter 2 gave you the personal operating system — the mindset that determines whether everything else sticks. Chapter 3 gave you the organizational blueprint — how individual action becomes collective behavior. And this chapter has given you the strategic architecture: where the industry actually is, why pilots stall, what the regulatory environment requires, how Microsoft 365 Copilot is built for exactly this environment, what risks to manage and how, what organizational structure enables scale, and what the economics look like.

You now have the complete map.

Part II of this book — beginning with Chapter 5 — is where you start driving.

We go application by application, workflow by workflow, through the Microsoft 365 Copilot suite: Word, Excel, PowerPoint, Teams, OneNote, SharePoint. Not conceptually. Hands-on. In your actual Microsoft 365 environment, doing real work, building real habits.

The strategy in Part I becomes the practice in Part II. And the practice becomes the Showcase Project in Part IV.

The foundation is solid. The road ahead is clear.

Let’s build.

AI Center of Excellence (CoE) A lightweight organizational coordination function that prevents AI adoption from fragmenting into disconnected departmental initiatives — maintaining shared governance, shared learning, and shared standards across the institution.

Microsoft Graph The technical data layer underlying Microsoft 365 that connects all M365 services into a unified model of a user’s work activity — enabling Copilot to synthesize across email, calendar, documents, and Teams conversations contextually.

Work IQ Microsoft’s applied intelligence layer built on the Microsoft Graph — enabling Copilot to answer contextual questions about a user’s actual work environment without requiring manual data loading or specification.

Model Risk Management (MRM) The OCC-regulated framework governing AI and statistical models used in material banking decisions — requiring validation, documentation, ongoing monitoring, and governance.

Permission Inheritance The architectural principle by which Microsoft 365 Copilot respects existing M365 access controls — ensuring the AI can only surface data that the requesting user is already authorized to access.

Hallucination The AI phenomenon in which a model generates factually incorrect information with apparent confidence — a known limitation of large language models that requires human verification of all factual outputs in material contexts.

Valley of Death The organizational phase between a successful AI pilot and enterprise scaling — characterized by governance review queues, fading momentum, and the absence of structural mechanisms to convert pilot results into repeatable patterns.

AI Adoption One-Pager A single-page personal implementation plan identifying the specific workflow, current state, AI-assisted future state, metrics, and risk controls for a professional’s first AI deployment — the seed of the Showcase Project.

Microsoft Purview Microsoft’s compliance and data governance platform — providing audit logging, data classification, information protection, and compliance management for all Microsoft 365 activity including Copilot interactions.

Proportional Governance The principle that AI governance intensity should be calibrated to the risk level of the specific use case — enabling a fast lane for low-risk productivity use while applying full regulatory scrutiny to material banking decisions.